|

Corresponding author: Philip Wallage ( p.wallage@vu.nl ) Academic editor: Chris D. Knoops

© 2018 Philip Wallage, Jan Bouwens, Olof Bik.

This is an open access article distributed under the terms of the Creative Commons Attribution License (CC BY-NC-ND 4.0), which permits to copy and distribute the article for non-commercial purposes, provided that the article is not altered or modified and the original author and source are credited.

Citation:

Wallage P, Bouwens J, Bik O (2018) The view from practice: Improving audit quality is a joint responsibility. Maandblad Voor Accountancy en Bedrijfseconomie 92(7/8): 197-200. https://doi.org/10.5117/mab.92.30344

|

Cross-border collaboration in the auditing profession is key for improving audit quality: not just between academia and practice, but also between audit firms on the one hand and clients, regulators and policy-makers on the other hand. The auditors themselves must do a better job, but clients and other stakeholders will also have to take responsibility for the collective challenge the profession is facing: enhancing audit quality and restoring societal trust. In a nutshell, this was the view from practitioners in the auditing profession during the 3rd International Conference of the Foundation for Auditing Research (FAR), June 2018. In this paper the discussions during the Conference about the need for further collaboration between academics and practitioners and the way this could be organized, are presented.

1. Across the full spectrum of the profession

Practitioners were well represented in the 140-strong audience. The ratio between practising professionals and academics was broadly fifty-fifty, the same goes for the ratio of auditors working in (major) firms and within the broader business community. These conference statistics indicate that practitioners are getting more and more involved in academic discussions about the continuous development of the audit profession to boost quality. The voice from practice was also clearly heard in the discussion between the diversely composed panel and the representatives of the audit firms and other conference participants. Or, in the words of conference chair Willem Buijink, professor at the Dutch Open University and previously at Tilburg University: “We have started to collectively look for the driving forces of audit quality, across the full spectrum of the profession”.

2. Performance and expectations gap

This ‘full spectrum’ was neatly present in the panel of four, consisting of the CEO of an audit firm (Anneke van Zanen, Baker Tilly Berk), a board member of the Dutch professional body of accountants, NBA (Marco van der Vegte), an academic (Marleen Willekens, professor Accounting and Auditing at KU Leuven) and a lawyer, for the much needed outside perspective on the audit profession (Monique van Dijken-Eeuwijk, NautaDutilh). Outsiders usually have a keen eye for complex issues and a more impartial view. So not surprisingly, it was Van Dijken-Eeuwijk who pinpointed the root cause of the ongoing struggle in the audit sector. In her view: “The debate about audit quality is due to a lack of trust. In order to remedy this, it’s imperative that all actors recognize their responsibility: not just individual auditors, but also the audit firm, the client, the audit committee and supervisory board, and the Dutch regulator Authority for the Financial Markets (Autoriteit Financiële Markten)”. According to Van Dijken-Eeuwijk, the profession is experiencing not only a performance gap, but also an expectations gap: society’s expectations are too high. Transparency and highlighting shared responsibility will play a significant role in bridging these gaps, Van Dijken-Eeuwijk said. All stakeholders must collectively form a cross-sectoral ‘chain’ for improving audit quality and restoring societal trust. Henriëtte Prast (professor at Tilburg University and chair of FAR) took a similar stance: “Improving quality has to be focused on society as the most important stakeholder”.

3. Client can be auditor’s ally

The need for a heightened sense of joint responsibility for audit quality was demonstrated by some studies of FAR research teams, which were presented at the conference. Preeti Choudhary (University of Arizona) for instance, found that in nearly half of the studied cases clients refrained from making adjustments to the financial report, which were proposed by their external auditor because of mistakes or misrepresentation. Only in 12 percent of the cases all proposed adjustments were made. “So clients aren’t always listening to the auditor, although they should both be committed to the reliability of reporting”, was one of the remarks in the audience. The contribution of Mark Peecher (University of Illinois) on timely detection of fraud by alertness of auditors to hidden signals during earnings calls, elicited another comment from a representative of the audit firms in the audience. Michael de Ridder, globally responsible for audit quality at PwC, stated: “The responsibility for fraud is transferred unilaterally to the auditor, which is inequitable. There needs to be a broader discussion on what companies themselves should be doing to prevent fraud attempts or flag these in time. Regulations ought to be focused on the client as well as the auditor”. De Ridder pre-empted with a practical suggestion: “Each and every company should get a fraud officer”. Peecher nodded assent: “The client can be the auditor’s ally”.

4. Let each actor formulate its own drivers of audit quality

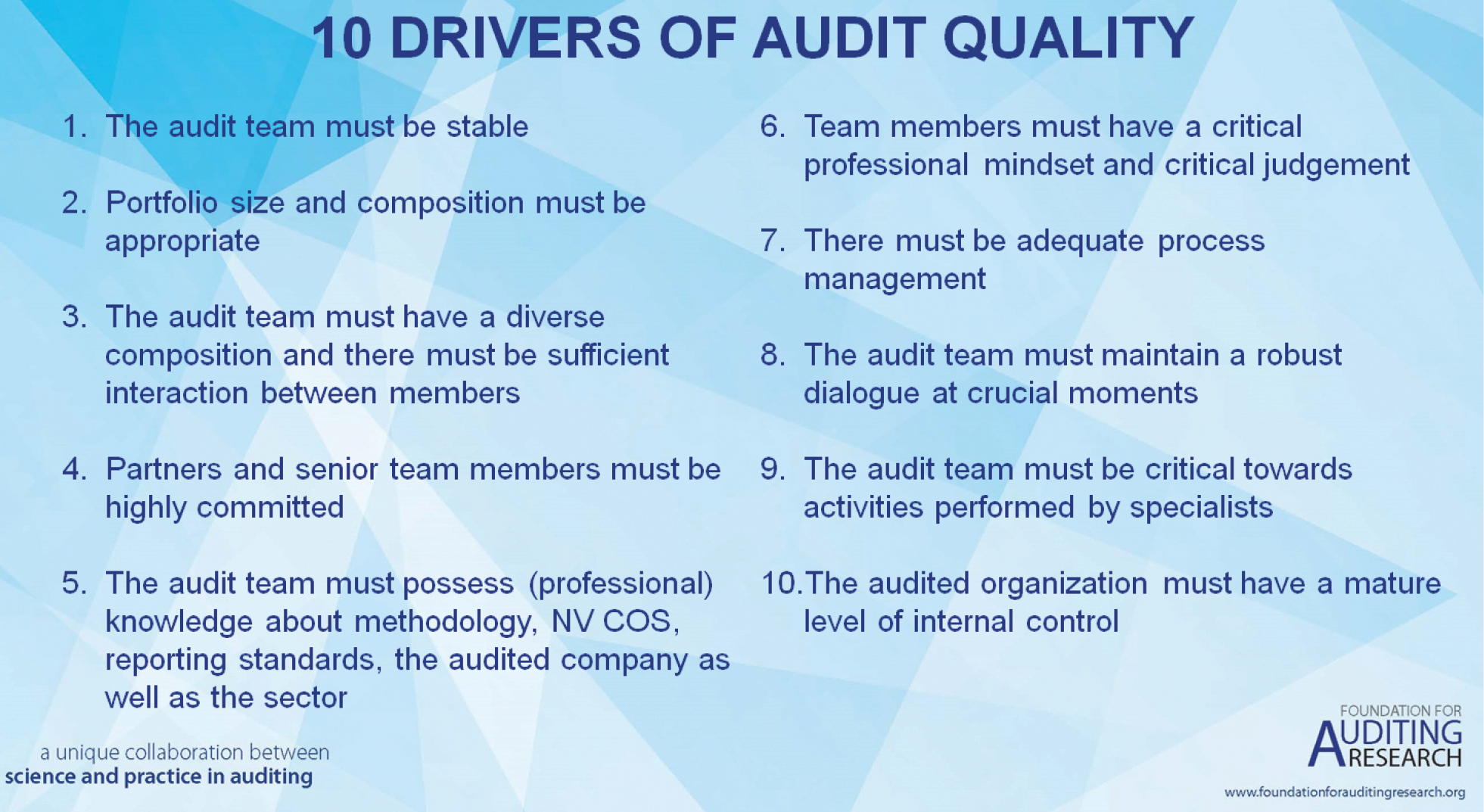

Allies are important in reflecting on public criticism in strengthening audit quality. During the panel discussion Van der Vegte was the first at the conference to point to the recently issued second report of the Monitoring Committee Accountancy. The report has the tantalizing title Doorpakken! (Press Ahead!). Reforms in the profession need to be implemented more swiftly and with more far-reaching effect, the committee concluded. Van der Vegte himself was involved in the recently published 10 drivers of NBA’s professional root-cause analyses of the drivers of audit quality – one of the earlier 53 recommendations of the NBA. The recently published 10 drivers constitute the outcome of that analyses and are supported by the Big Four and the Next Five, Van der Vegte said.

The 10 drivers of audit quality solely focus on the audit profession. But if audit quality is a broader, joint responsibility, all actors should draw up their own list of 10 drivers for quality, Van der Vegte stated: “not just us as auditors, but also clients, regulator AFM and the public at large”. The current quality drivers are primarily intended for audit teams. “What might the list look like for those other actors, starting with the executive boards of audit firms?”, a conference participant asked. Van der Vegte answered: “At board level criteria for quality are for instance the organization’s purpose, the tone at the top and the way management handles dilemma’s like: do we put society’s interest or the partner’s interest first? Client acceptance would also be a focal point”. At the profession’s level, the availability of people with the right competences and mindset is the most significant driving force for quality: “Is the audit profession still capable of attracting those people?” Van Dijken-Eeuwijk implicitly indicated earlier what the quality criteria might be for clients’ management (quality of reporting, focus on long term value creation and business continuity, and fraud prevention), the supervisory board members (quality of supervising reporting and risk management), and regulator AFM (quality of external monitoring and safeguarding trust).

5. “You don’t need to score a 10”

“How can you be sure that you’ve done a good job as auditor?”, was another question from one of the conference participants. Van der Vegte: “Quality can be measured against hard criteria, such as how well the engagement management team is functioning, how many hours have been spent on the audit assignment, et cetera. But you can also look at soft factors, such as the interaction between team members. The quality of cooperation for instance can be measured by instruments as 360-degree feedback”. Perhaps quality can also be measured by means of client satisfaction, suggested Willekens, although client satisfaction is not per definition equal to audit quality and societal trust. “80% of clients are delighted”, responded Van Zanen. “Even though AFM’s figure gets stuck around 60-70%”. However, clients use different criteria for quality, Van Zanen stated. “One thing clients deem important is being able to have a good dialogue with their auditor”. Hence there is a variety of perspectives when it comes to quality, is the conclusion. “You end up encountering the expectations gap again”, Van Dijken-Eeuwijk remarked. “Some expectations just can’t be fulfilled by auditors. The expectations gap is a fair bit harder to manage than the performance gap”. Van Zanen: “We keep talking about society’s lack of trust in the profession. If you keep repeating that in the press, then it becomes a self-fulfilling prophecy. Auditors work hard to raise the quality from the current seven to an eight. You really don’t need to score a 10. Nobody is expecting that. That would make the audit far too expensive”.

6. Diversity also has a downside

The panel discussion turns to the topic of diversity. Willekens zooms in on the relationship between audit quality and the structure of audit teams. She makes a distinction between two dimensions of diversity: underneath the surface of a mixed composition in terms of demographics, hierarchy and discipline, lurks a deeper form of diversity: different roles, knowledge, and expertise. With this hidden form of diversity, group dynamics, pecking order, mutual trust, and common goals come into play. Van Zanen is a hands-on expert on both dimensions of diversity. As CEO of Baker Tilly Berk she is the only woman among 43 male partners. Her view on the first diversity dimension: “Men have made the organization great, but now change is required and to that end we need diversity at each and every level, not only in the audit teams but also at the top. We therefore have to attract different people and give them the room that will enable them to literally make a difference”. That is a little too simplistic for one conference participant: “How do you succeed in attracting those different people?” In her answer Van Zanen highlighted the importance of recruitment and selection committees with a diverse composition. “If they are only made up of grey-haired Dutchmen over 55, there’s a good chance they will select grey-haired Dutchmen over 55”. Van Dijken-Eeuwijk has another suggestion: “Speaking about the purpose of the organization will attract younger people”. Diversity is broader than just sex, age or ethnicity, it is also about different backgrounds, remarked another conference participant. Van der Vegte nodded assent: “As an auditor you also need to be open and make yourself vulnerable to disciplines such as IT, psychology and forensics, for instance”. That doesn’t always come naturally, according to Willekens. “Research shows that people from different disciplines are sometimes regarded as outsiders. Hence there’s also a downside to diversity”.

7. Shared dream

How can the second dimension of diversity boost audit quality? Van Zanen compares audit teams with sports teams. “You win the match with the best team, not with the best players”. Forging that team is something you do with “a shared dream, with common goals, with luck, passion, and the will to achieve something together”. This calls for commitment from each and every team member: “They all have to have the same drive and appetite for quality”. But it is not just about excellence: effective teams are also built on respect. “The upper echelons need to respect the lower levels”, underlines Van Zanen. Communicate respectful and listen properly, is her advice: “Let people surprise you, be open to their ideas”. However difficult that may be.

8. Wanted: grey hair

Within audit teams this asks for better cooperation and more communication - based on mutual respect - through hierarchical levels and between different age groups. For instance between juniors and more experienced team members, representing ‘grey hair’. The importance of and need for the latter was stipulated during the conference by Nico Pul, EY Executive Board member responsible for quality. Pul emphasized that having ample experience in teams is paramount: for audit quality as well as for helping mature young generations in the audit profession. Unfortunately, accumulating this much needed experience is increasingly threatened: standardisation and regulatory burden pushes the audit profession back towards a sharp focus on procedures and efficiency in the profession’s lifecycle. Whereas audit professionals want to develop themselves in the opposite direction during their careers: from standard knowledge to learning on the job, professional judgment and problem solving. This leads to a mismatch between the direction the audit profession is heading and the required journey of young talent, that is needed to help reform the profession and reinforce audit quality. This gap will also have impact in the future. Developments like artificial intelligence will never be able to completely replace auditors, Pul states. “Professional judgment, knowing the client and asking the right questions, will remain of the utmost importance. So experience, ‘grey hair’, will always be an indispensable part of our profession”.

9. Holding up a mirror

Let’s go back to the profession-wide responsibility for audit quality and the need to intensify collaboration between the audit profession and all the actors in the stakeholder field. Peter Hopstaken, Head of Audit from Mazars, one of the Next Five audit firms, stressed the importance of objective, independent research in this respect. “It is bolstering discussions and decision-making on the future of the audit profession and holding up a mirror in an era in which trust of society, government, and other stakeholders is under pressure. But it’s also providing stakeholders with insight into how the audit profession is working towards improving quality, based on data from the heart of the auditing practice, supplied by audit firms themselves”. The latter is creating important added value by FAR, although it also presents a challenge for both academics and the Big Four and Next Five. After all, research consumes scarce time and capacity and requires a robust reciprocal effort to define and amass data and deliver them on time for the researchers. “It’s a learning curve, but as a profession and as academics we are on the right track”, Hopstaken concludes.

10. Inspiration for leaders

“Are we actually moving the profession forward?” It was Bert Albers, managing partner of Deloitte Netherlands, who dared posing the key question, alluding to the title of the conference as well as FAR’s mission. The answer is a resounding yes, according to Albers. “I’ve taken a lot of inspiration for my role as audit leader. Once again it has reconfirmed to me that we’re focusing on the right topics in day-to-day practice”. The budding relationship between practising professionals and academics is now taking off, Albers added. “Something beautiful is blooming. We’re not there yet, but we are making great progress”. His quote of philosopher Jürgen Habermas was highly applicable: “Only by externalization, by entering into social relationships, can we develop the interiority of our own person”.

This takes us straight back to the Leitmotiv of the conference: the audit profession must improve audit quality, but cannot do so alone. This interdependency is again neatly encapsulated in a quote from polymath Benjamin Franklin: “We must, indeed, all hang together or, most assuredly, we shall all hang separately”.

Prof. dr. Ph. Wallage RA is a professor of Auditing at Vrije Universiteit Amsterdam (VU) and Universiteit van Amsterdam (UvA).

Prof. dr. J.F.M.G. Bouwens is a professor of management accounting at the University of Amsterdam and Managing Director of the Foundation for Auditing Research.

Prof. dr. Olof Bik RA is a professor of Behavioral Research in Auditing at Nyenrode Business University and Managing Director of the Foundation for Auditing Research.